SAP is the leading enterprise ERP vendor worldwide. The company started in 1972 in Germany, creating software for mainframe computers, and since then, it expanded into a comprehensive spectrum of products for SMBs, mid-market, and enterprise customers. SAP went public in 1988 and now offers ERP, manufacturing, financials, SCM, HCM, CRM, commerce, data and analytics solutions.

SAP has more than 110,000 employees, $37 billion in revenues (USD), 7% of which is services revenue, and approximately 27% in operating income. It has more than 425,000 customers in more than 180 countries, including more than 80% of the Fortune 500.

The company historically had on-prem offerings, but in 2017, it launched its S/4HANA Cloud product, which continued its adoption and now is 11% of overall revenue (cloud revenue has grown to approximately 44% of SAP’s overall revenue). Similar to Adobe’s transformation into a cloud-first, recurring revenue company, SAP successfully continues to convert its business to a more predictable subscription revenue stream. Worldwide, TAM for SAP’s platforms is around $500 billion.

Implementing SAP solutions requires customization and professional services. Like other ISV platforms, SAP wants to limit its exposure to professional services revenue to maintain a software-centric financial profile. Therefore, SAP has communicated that it wishes to rely more on service partners to assist with its cloud revenue growth. SAP partners with comprehensive offerings are expected to generate up to $7 for every $1 of SAP revenue.

We wanted to learn more about the SAP services partner ecosystem and analyzed what we could find from their public partner data. SAP has a mature partner program with approximately 2,960 partners, of which around 2,100 are service partners, employing more than 6,700,000 employees worldwide.

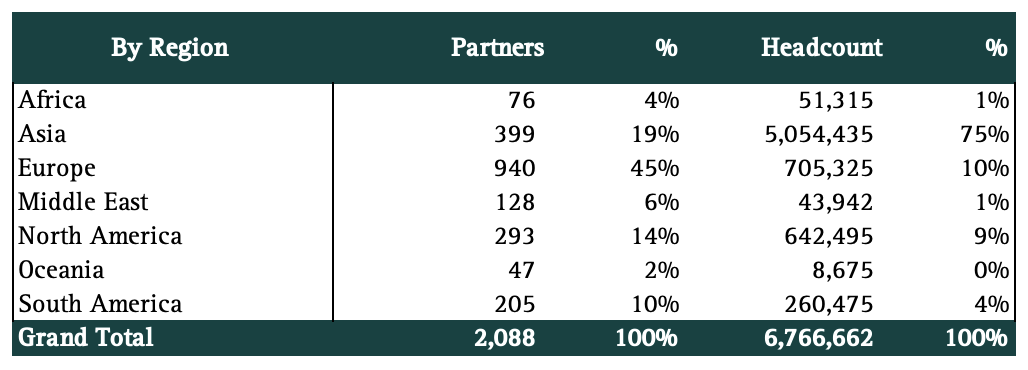

The above table summarizes the service partner data we collected. The regional data should be interpreted as to where the partner headquarters is located and, secondarily, where most of their headcount is based. Regardless of the partner’s HQ location, notice the high percentage of Asian talent (75%) primarily driven by Indian-based employees of these services organizations. Given SAP's heritage, we can also see a high proportion of European-based partners.

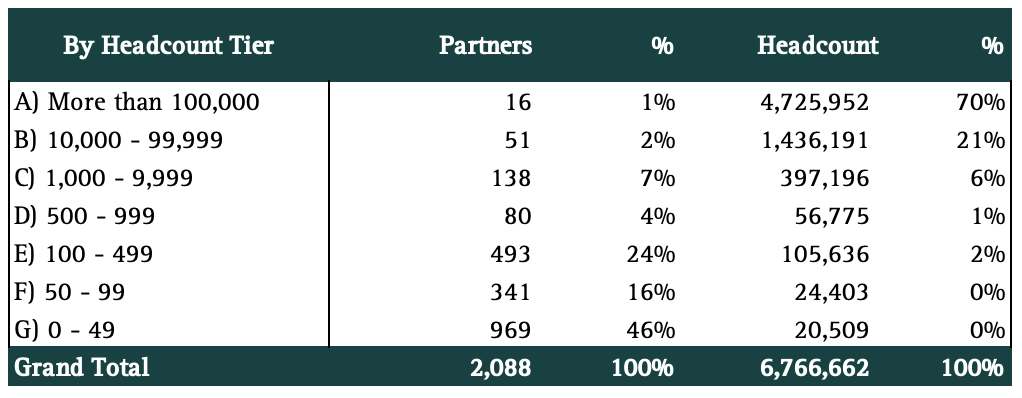

In terms of partner size, almost 1,000 partners have fewer than 50 employees, and 86% of worldwide partners (1,800+) have fewer than 500 employees. There is important fragmentation among smaller-sized SAP service partners.

At Alten Capital we invest in business and technology services companies. Supporting ISV ecosystems has proven to be a viable strategy for scaling niche services organizations. Please reach out to us to explore partnership opportunities.